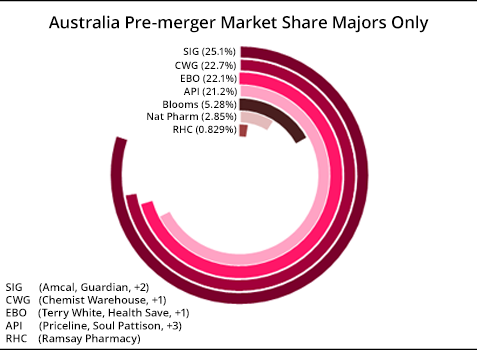

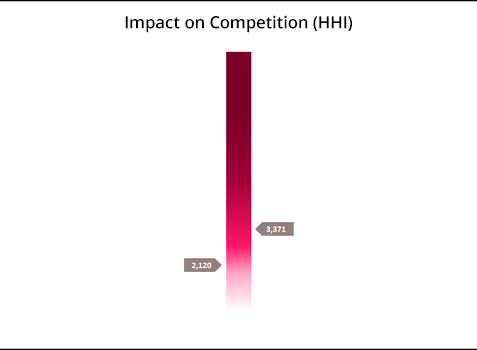

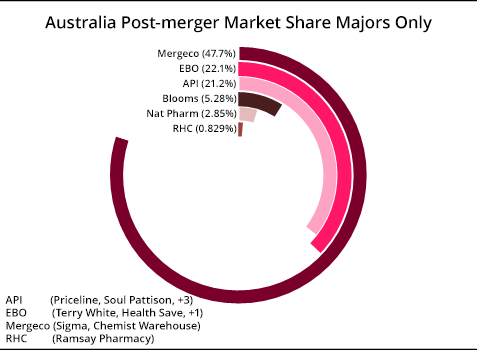

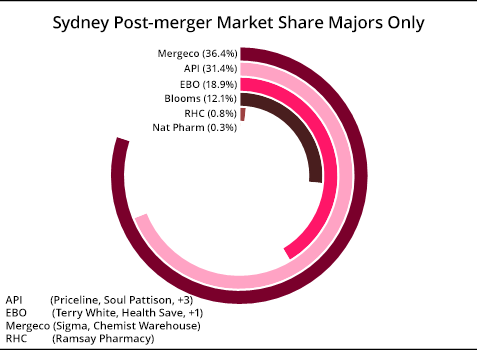

Majors Only

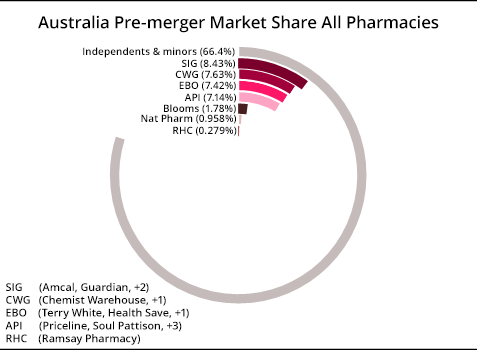

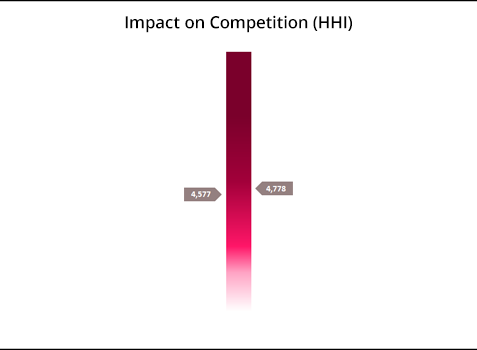

Australia

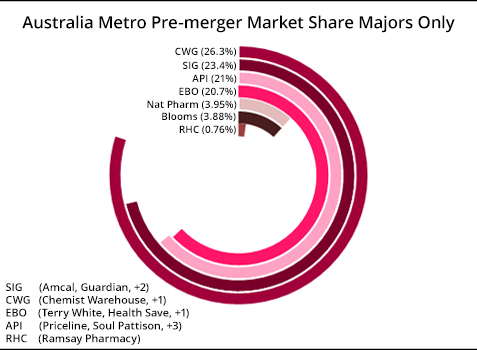

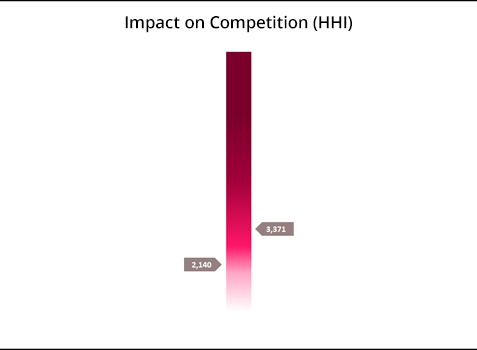

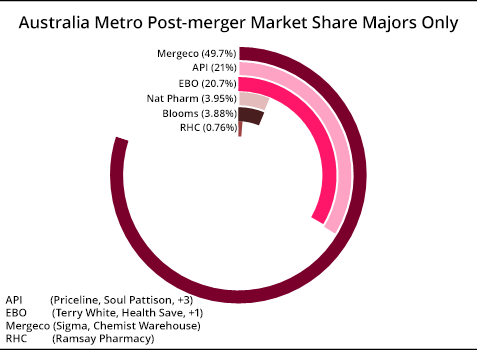

Australia Metro

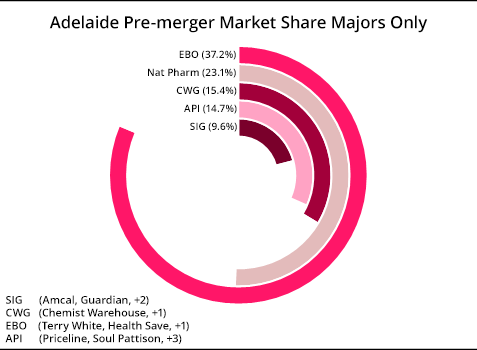

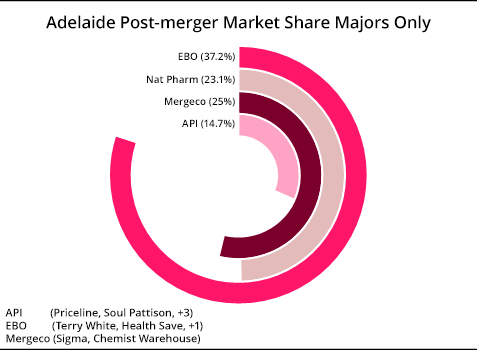

Adelaide

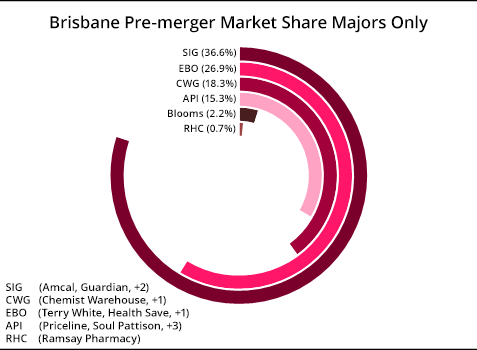

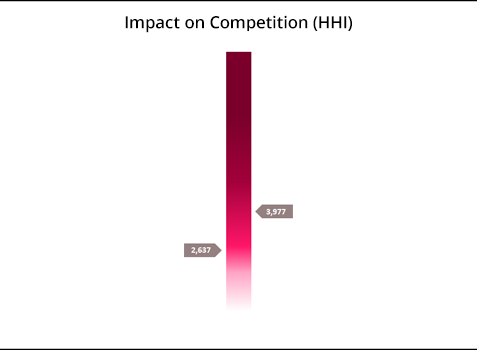

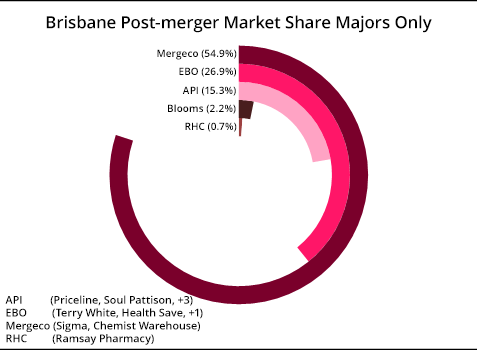

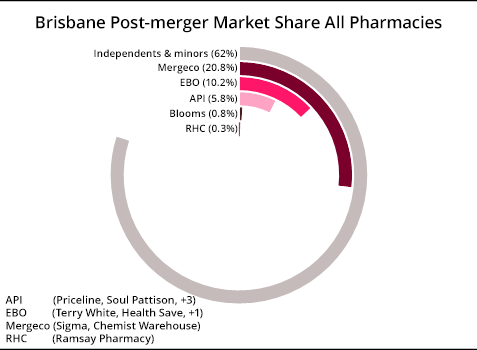

Brisbane

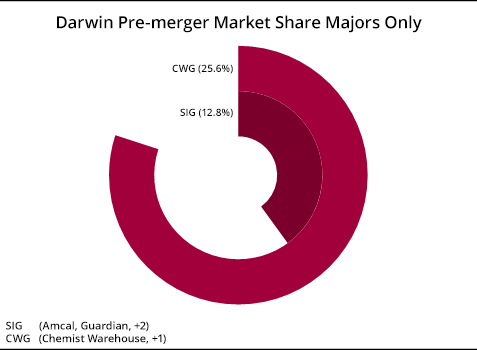

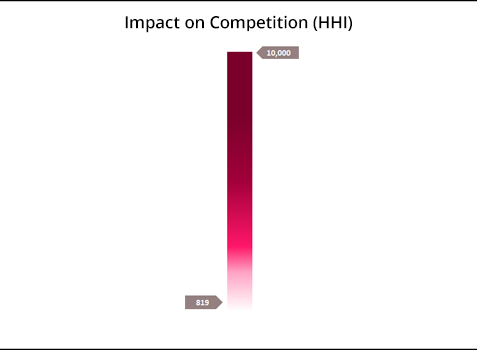

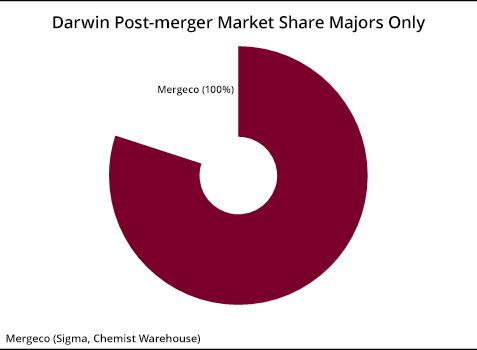

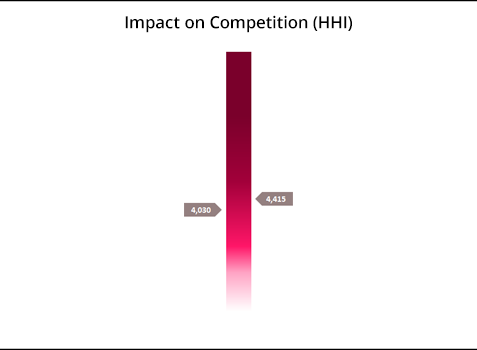

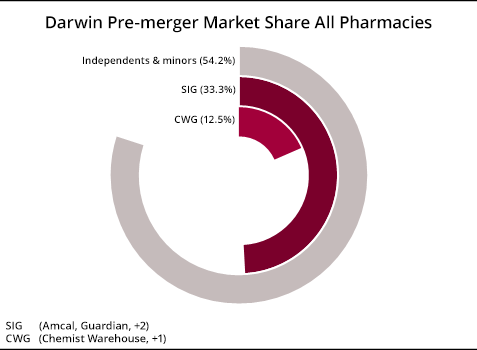

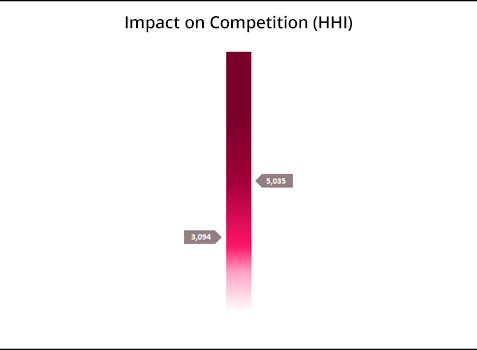

Darwin

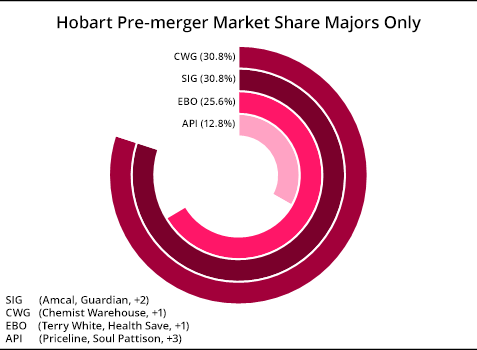

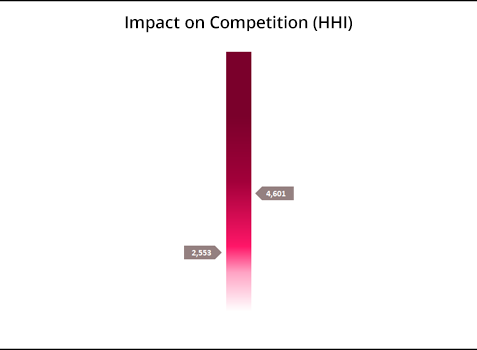

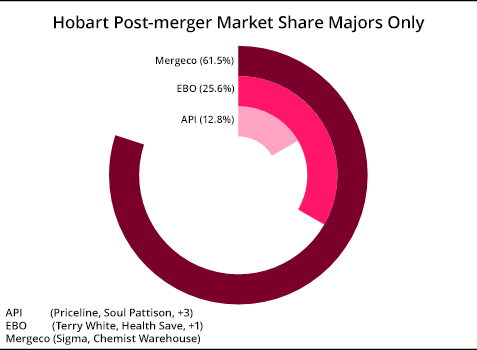

Hobart

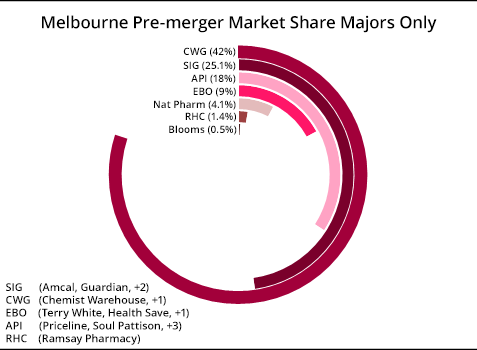

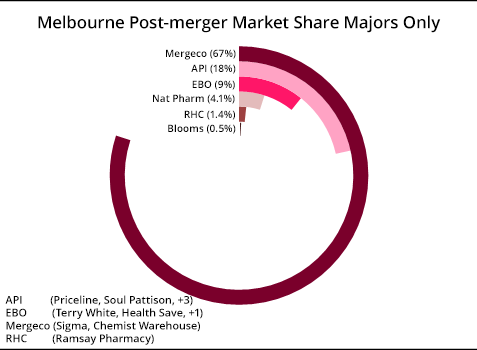

Melbourne

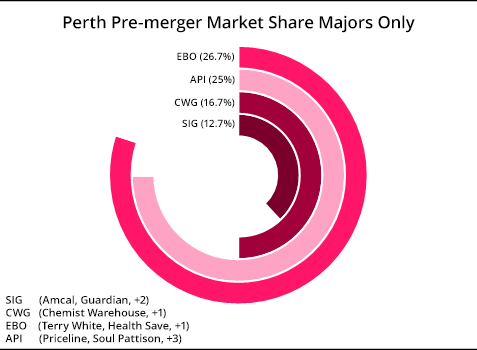

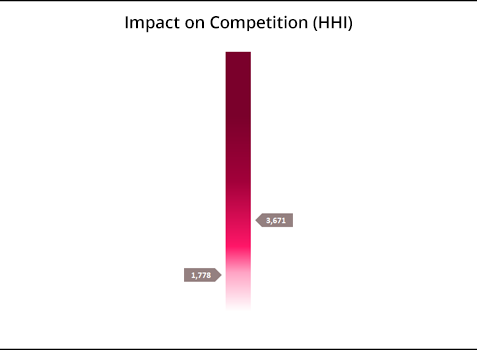

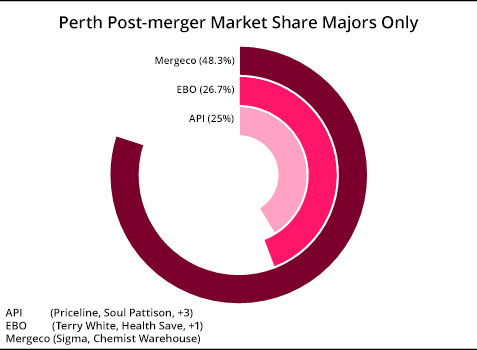

Perth

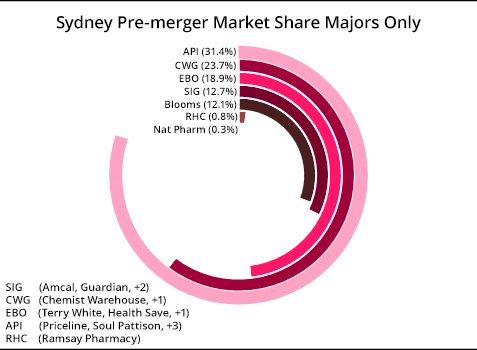

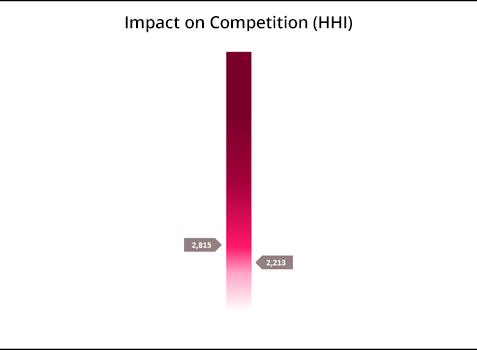

Sydney

All Pharmacies

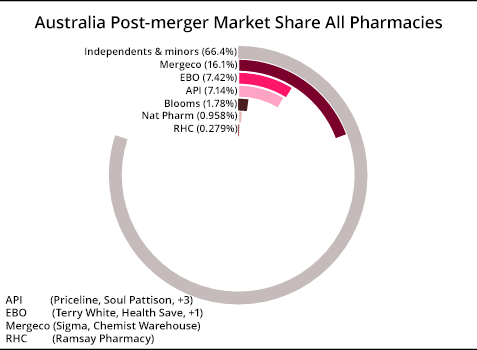

Australia

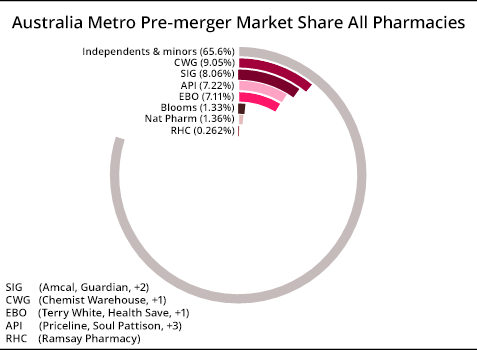

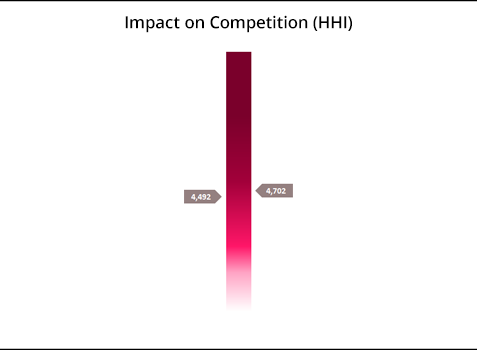

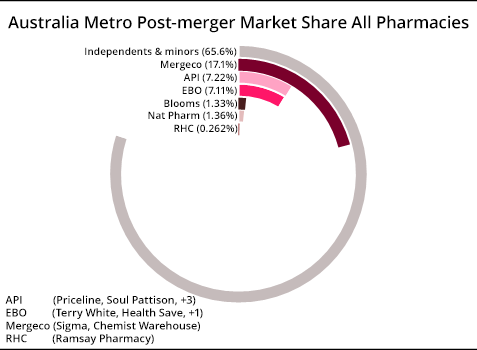

Australia Metro

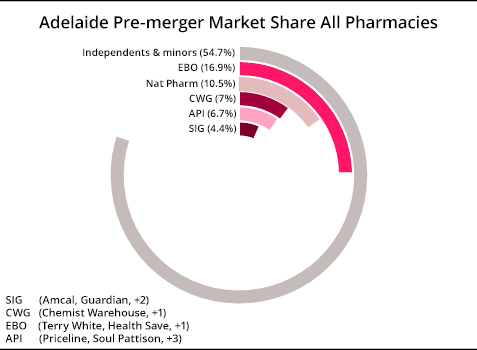

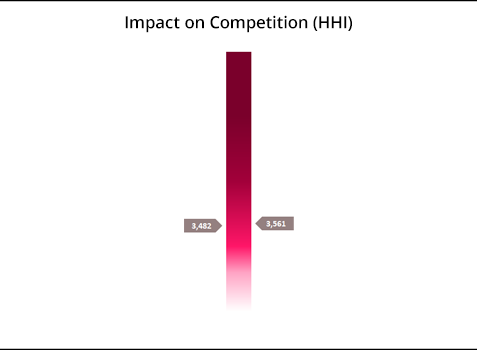

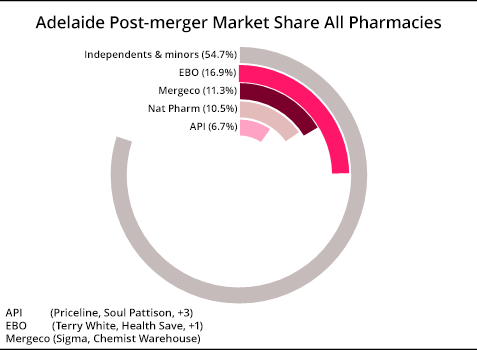

Adelaide

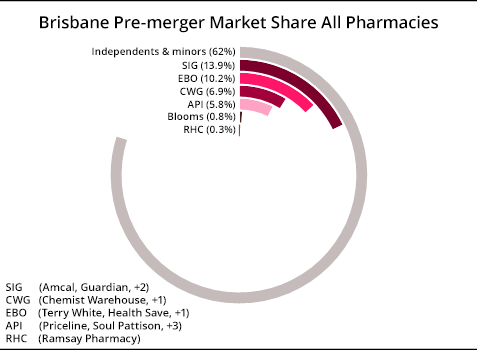

Brisbane

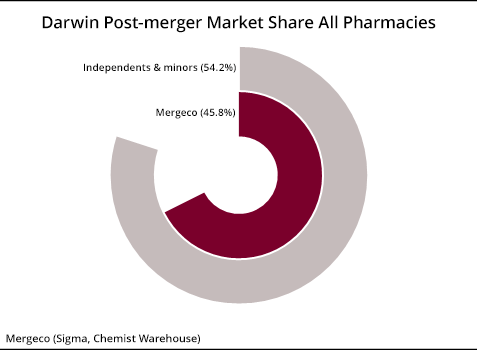

Darwin

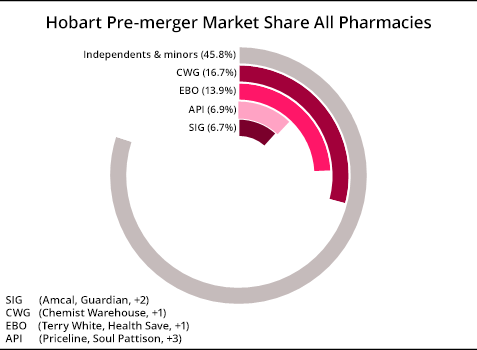

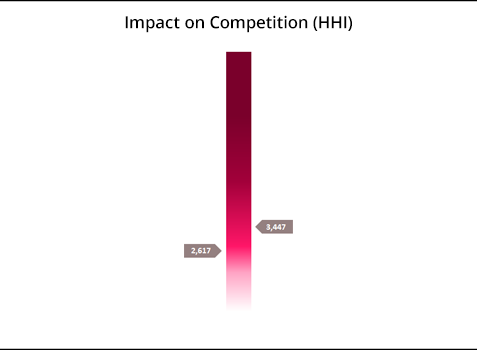

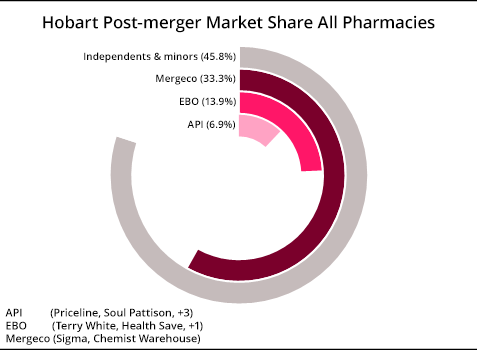

Hobart

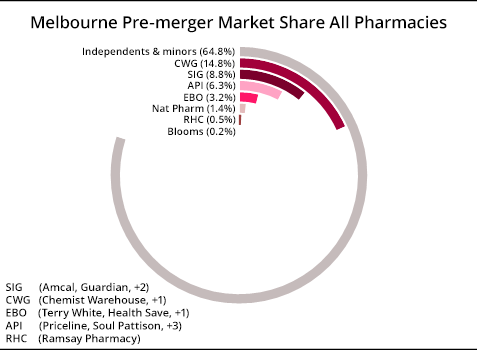

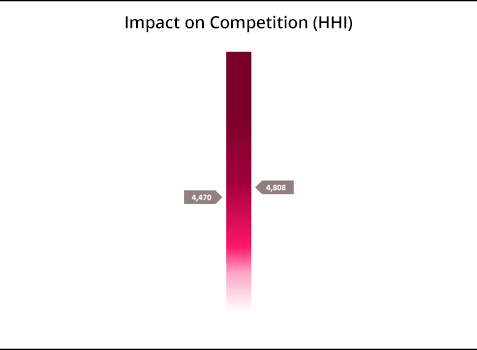

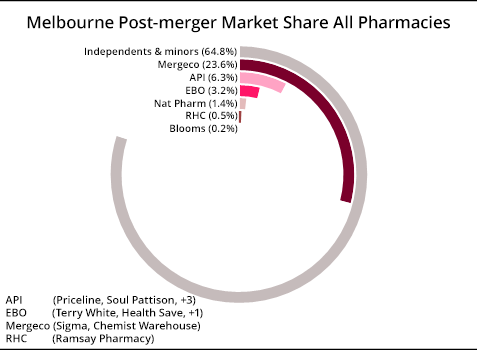

Melbourne

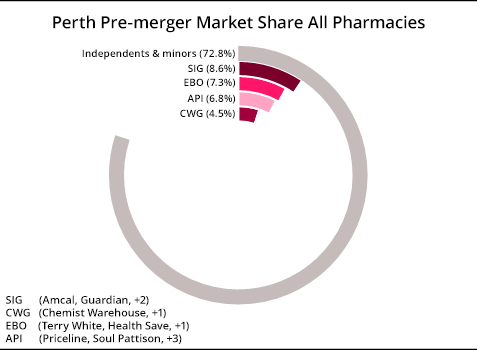

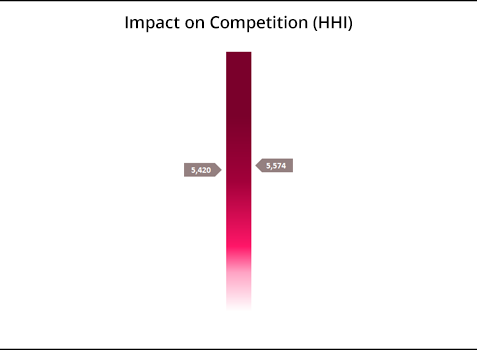

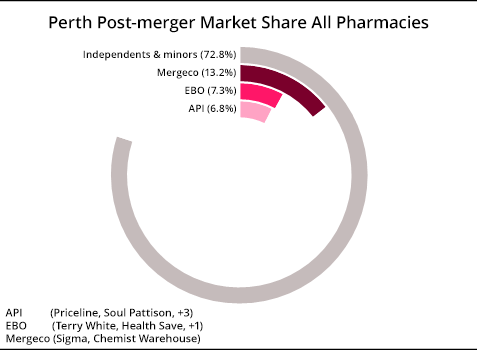

Perth

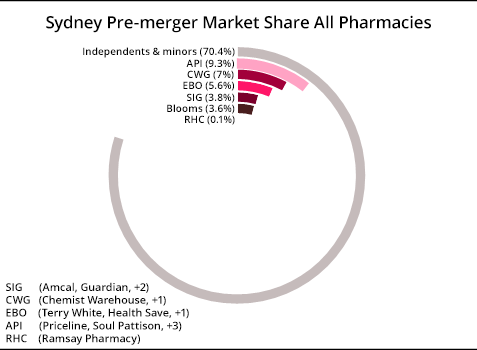

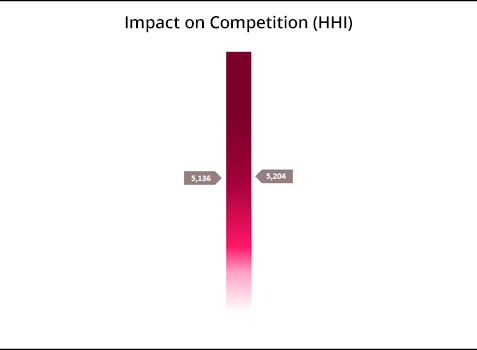

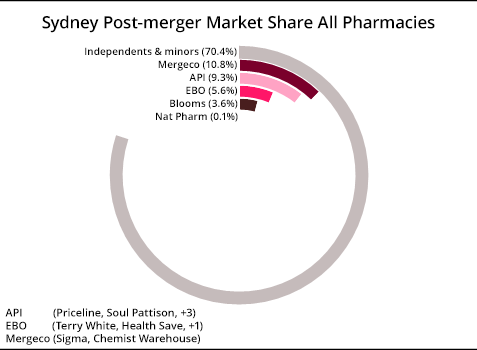

Sydney